Gold has a way of showing up in investment conversations at very specific moments. Inflation headlines rise, markets fall sharply, and geopolitical risk dominates the news cycle. In those moments, gold is often presented as a timeless solution, something that will protect purchasing power, stabilize a portfolio, or provide safety when other assets feel uncertain.

At Keen Capital, we work with high-net-worth individuals and families to invest and manage their wealth over the long term. When gold comes up, the question is rarely about curiosity. It is usually about reassurance. This article looks at whether to add gold in your portfolio, if it actually does the job many investors expect it to do, and how to think about it within a well-constructed portfolio.

The Question Behind The Question: What Job Do You Want Gold To Do?

Before asking whether gold belongs in your portfolio, it helps to ask a more specific question. What role do you want it to play?

Most investors are looking for one of three things: they want protection against inflation, something that holds up in market stress, or diversification that smooths overall portfolio volatility.

The challenge is that gold does not consistently deliver all three, and it does not generate cash flow. Stocks have earnings. Bonds have interest. Real estate produces income. Gold relies almost entirely on price appreciation driven by sentiment, demand, and macro conditions. That makes its expected return harder to define.

If you find it hard to articulate the role you want gold to fulfil in your portfolio, it is a sign that the decision may be driven more by headlines than by planning.

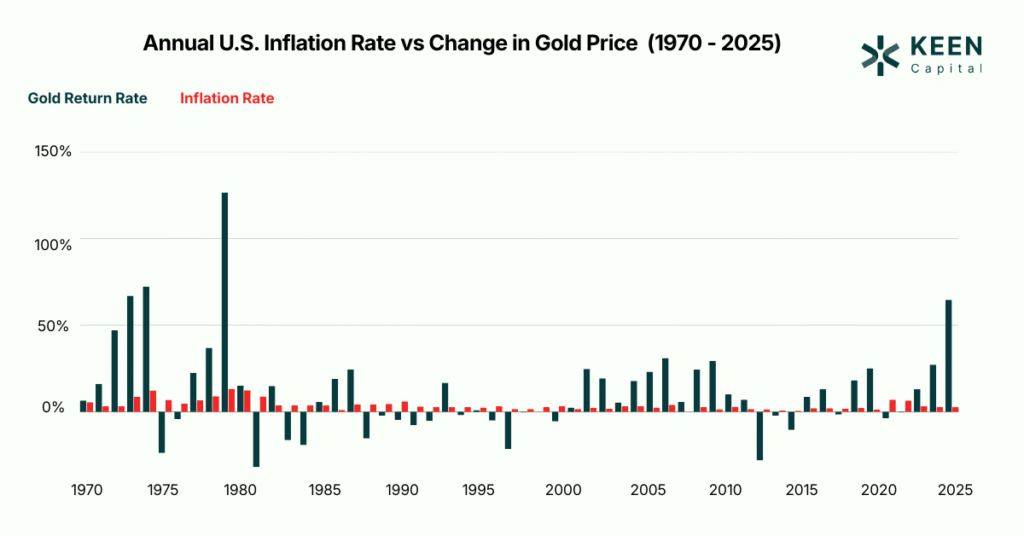

What The Data Says About Gold As An Inflation Hedge

Gold is often described as an inflation hedge, but the evidence is mixed, especially over the timeframes that matter most to investors.

Over very long periods, gold has sometimes kept pace with inflation. Over shorter periods, which is when inflation feels most painful, gold has been inconsistent. There have been extended stretches where inflation rose meaningfully, and gold prices lagged or declined.

For investors who care about protecting near and medium-term spending power, this matters. Tools like Treasury Inflation Protected Securities and I Bonds are explicitly linked to inflation and provide a clearer mechanism for matching assets to future liabilities. Gold does not have that direct linkage.

This does not mean gold can never help in an inflationary environment. It means relying on it as a primary inflation hedge introduces uncertainty at exactly the wrong time.

Does Gold Really Protect You In Bad Times?

Gold’s reputation as a safe haven is rooted in history, but the reality is more nuanced.

There are periods when gold has held up well during equity market declines. There are also periods when it has been volatile or moved in the same direction as risk assets. Its behavior depends heavily on the nature of the crisis, the source of stress, and the broader macro environment.

During liquidity-driven events, when investors sell assets broadly to raise cash, gold can fall alongside stocks and bonds. Even when gold does help, the ride can be uncomfortable. Sharp swings are common, which can be difficult for investors who may need to rebalance or fund spending during stressed markets.

Rather than asking whether gold protects against “bad times” in general, it is more productive to define the risk you are actually worried about. An equity market crash, an inflation spike, stagflation, or a liquidity crunch all call for different portfolio tools.

The Case For Gold And Its Limits

The strongest argument for gold is diversification. At times, gold behaves differently from stocks and bonds, which can help reduce overall portfolio volatility.

However, diversification is not guaranteed, and it comes at a cost. Gold does not produce income, and it can underperform for many years at a time. When that happens, investors face an opportunity cost. Capital tied up in a non-productive asset is capital not earning returns elsewhere.

In portfolios that already include high-quality bonds, inflation-linked securities, broad equity exposure, and a properly sized cash reserve, the incremental diversification benefit of gold is often modest. The trade-off is increased complexity and a higher chance of behavioral mistakes when gold inevitably goes through a rough period.

Keen Capital’s View: Why We Generally Do Not Include Gold

At Keen Capital, we generally do not include gold in client portfolios.

The reasons are straightforward. Gold can be extremely volatile, and its long-term expected return is unclear. The most common reasons investors cite for owning gold, such as inflation protection and crisis hedging, are not consistently supported by the data over the periods investors care about most.

When clients are drawn to gold, it is often a signal that something else in the plan needs attention. Liquidity may be too tight. Risk may be concentrated in one area. Or the portfolio may not be aligned with how spending and taxes will actually unfold over time.

In our experience, those issues are better addressed through thoughtful portfolio construction and planning rather than adding a single asset with an uncertain role.

If You Still Want Gold, Keep It Small And Be Explicit

Some investors will still want gold exposure, even after understanding the trade-offs. If that is the case, discipline matters.

Gold should be treated as a diversifier, not a return engine. That means setting a clear maximum allocation, committing to a long holding period, and defining rebalancing rules in advance. Many frameworks that do include gold keep it in the low single digits of a portfolio.

Without those guardrails, gold positions tend to grow or shrink based on emotion and headlines, which undermines the very stability investors hope to achieve.

There are several ways to gain gold exposure, each with its own considerations.

Physical bullion introduces storage, insurance, and liquidity concerns. Gold-backed ETFs are simpler to access but come with ongoing fees and track the same underlying volatility. Gold mining stocks are often mistaken for gold exposure, but they behave like equities with added operational risk.

Final Thoughts

Gold is often presented as a solution, but it is not a plan. It can diversify at times, but it is volatile, inconsistent as a hedge, and difficult to anchor to a clear expected return. For many investors, the comfort gold seems to offer can be better achieved through disciplined portfolio construction, tax and liquidity planning, and aligning investments with real-world spending needs.

At Keen Capital, our role as fiduciaries is to help clients make investment decisions grounded in evidence and long-term planning, not headlines. If you are questioning whether gold belongs in your portfolio, that is usually a signal that a broader review is worth having.

If you would like an objective second opinion on your portfolio, retirement strategy, or estate planning approach, we invite you to schedule a conversation.

We are happy to walk through your current structure, identify where risks and trade-offs actually sit, and help you decide whether changes are needed to better support your goals.