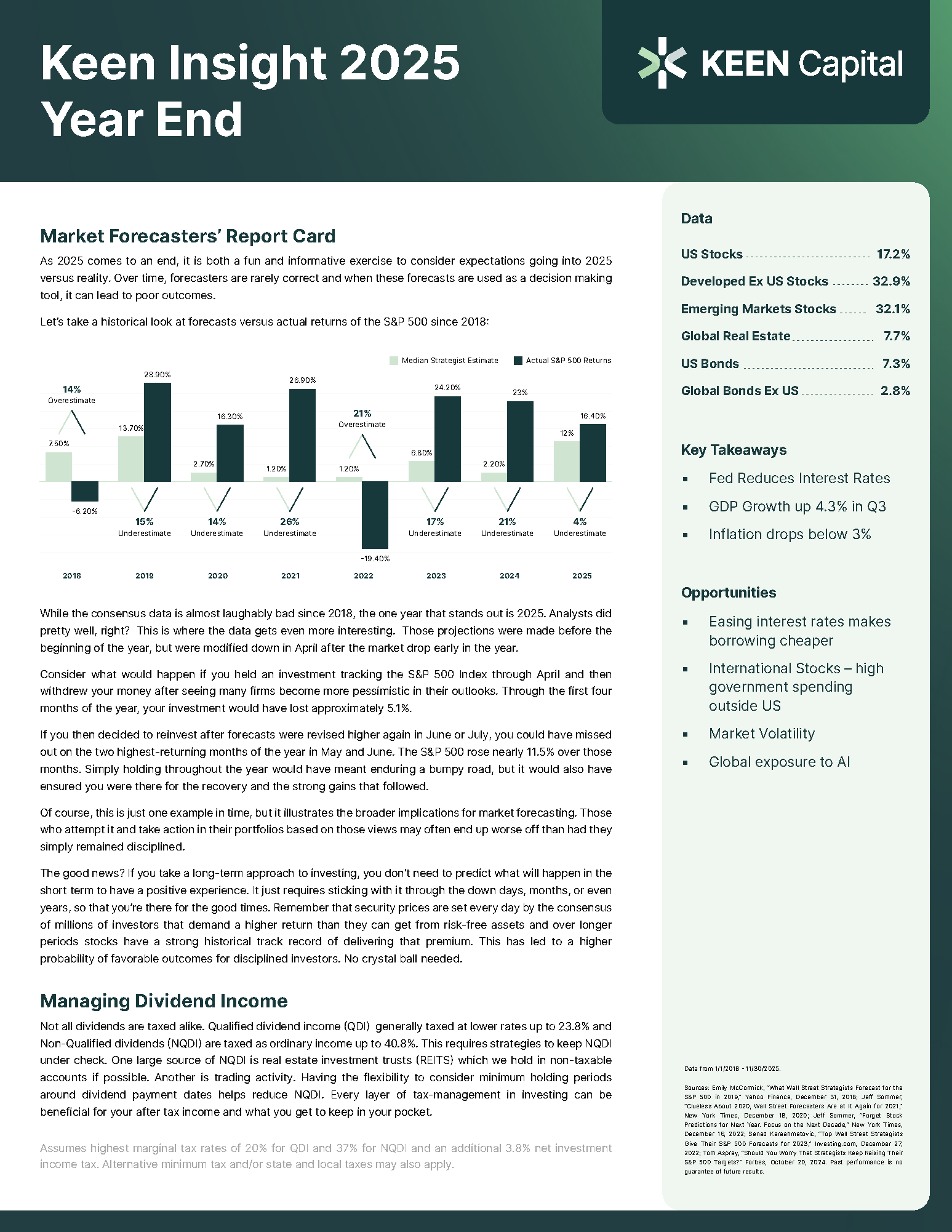

If you’ve saved and invested for years, it’s natural to assume that once you’re ready to use that money, you simply pull it out and spend it. But when it comes to taxes, not all withdrawals are created equal. The account you withdraw money from, Roth IRA, traditional IRA, or brokerage account, determines how much you actually keep in your pocket.

Understanding the withdrawal rules and how you’re taxed can make a huge difference over time. In this post, we’ll cover the IRA withdrawal rules and the nuances of each type of account, so you’ll know how to use them in your favor and keep more of what you’ve earned.

Roth IRA/401(k) Withdrawal Rules

Roth IRAs and 401(k)s are the most tax-friendly accounts in retirement. When you contribute to a Roth, you’re investing money that has already been taxed. That means when you withdraw those funds in the future, the earnings on top of your contributions can come out completely tax-free – if you follow the rules and if the rules don’t change.

To qualify for tax-free withdrawals, two things need to be true.

- First, you must be at least 59½ years old.

- Second, your Roth IRA must have been open for at least five years.

If you meet those requirements, every dollar of contributions and earnings comes out tax and penalty-free!

Before you reach those milestones, your original contributions are still accessible at any time without tax or penalty, because you already paid taxes on that money.

However, any earnings or investment gains withdrawn early are treated differently. If you pull out those earnings before age 59½ or before the account is five years old, that portion is generally subject to income tax and may also face a 10% early withdrawal penalty, unless you qualify for an exception, like certain education or first-home expenses.

No Required Minimum Distributions (RMDs) with Roth IRAs

Another major advantage of Roth IRAs is flexibility. They are not subject to Required Minimum Distributions (RMDs) during your lifetime. That means you can let the account keep growing for as long as you like, without ever being forced to withdraw money. For many retirees, that makes a Roth IRA a powerful tool for managing taxable income, leaving more control over when and whether you draw from it. It also provides a great legacy as taxes are already paid.

Tips for Roth IRAs Withdrawals

For high-income retirees, Roth IRAs can also be powerful planning tools. Because qualified Roth withdrawals don’t add to your taxable income, they can help you stay in a lower tax bracket, avoid triggering tax items based on income, such as higher Medicare premiums or Net Income Investment Tax (NIIT).

If you have a mix of account types, your Roth IRA comes in handy when you want extra income without pushing yourself into a higher tax bracket.

Traditional IRA Withdrawal Rules

Traditional IRAs work in the opposite way. You typically contribute with pre-tax dollars, which gives you a deduction when you contribute. The tradeoff is that every dollar you withdraw later is taxed as ordinary income. This is an important tool in your max earning years when your marginal tax rate is at its highest.

Let’s say you take out $100,000 from your traditional IRA in retirement. That full amount will be added to your taxable income for the year, and you’ll pay income tax on it at your current rate. If you withdraw before age 59½, you might also face a 10% penalty unless you qualify for an exception, such as using the funds for certain medical expenses, education costs, or a first-time home purchase.

Traditional IRAs come with Required Minimum Distributions (RMDs)

Once you reach a certain age, the IRS requires you to withdraw a specific percentage each year, whether you need the money or not. The idea is that since your contributions were tax-deferred, the government eventually wants to collect its share.

Tips for Traditional IRAs Withdrawals

Large withdrawals from your traditional IRA can push you into a higher tax bracket, which could also increase your Medicare premiums and taxes. To avoid this, many retirees spread withdrawals across multiple years or pair them with Roth conversions during lower-income years. Those over 70 ½ can also take advantage of Qualified Charitable Distributions (QCD) where contributions sent directly to charities are never taxed.

The key is balance. Use your traditional IRA for predictable income needs, but coordinate withdrawals carefully so you don’t end up paying more than necessary.

Brokerage Account Withdrawal Rules

A taxable brokerage account is often the most flexible, but it’s also the most misunderstood. Unlike your IRA accounts, you don’t get any tax deferral on what happens inside. You’re also not taxed for the act of withdrawing money itself. You’re only taxed when you realize income, like selling an investment for a profit, earning dividends, or collecting interest.

Here’s how it works in practice. If you sell an investment you’ve held for more than a year, you’ll likely qualify for the long-term capital gains tax rate, which is usually lower than your regular income tax rate. If you sell something you’ve held for a year or less, that profit is taxed as ordinary income.

Tax Treatment of Qualified vs Nonqualified Dividends

Dividends also come in two varieties: qualified and nonqualified. Qualified dividends meet certain IRS requirements and are taxed at the lower long-term capital gains rate (typically 0%, 15%, or 20%) depending on your income. For example, if you hold Apple stock and have owned it for more than 60 days around its dividend date, those payments count as qualified dividends, and you enjoy the lower rate.

Nonqualified dividends don’t meet those holding or issuer requirements and are taxed at your regular income rate. Common examples include dividends from REITs (real estate investment trusts), most bond funds, or stocks you held for only a short time before selling.

In short, qualified dividends reward long-term investors with lower taxes, while nonqualified dividends are treated like ordinary income.

Flexibility for Retirement or Generational Wealth Planning

Another advantage of brokerage accounts is flexibility. You can use strategies like tax-loss harvesting, which involve selling investments that have lost value to offset gains elsewhere. You can also control which shares you sell to fine-tune your tax bill. For example, selling shares with the highest cost basis can minimize your taxable gain.

And if you hold certain assets until death, your heirs may receive a “step-up in basis,” meaning they won’t owe capital gains on the appreciation that happened during your lifetime. For high-net-worth families, that can be an important part of long-term estate planning.

Withdrawal Planning Begins When You Start Investing

When it comes to withdrawing from multiple accounts, it’s easy to focus on what happens after you retire. But the truth is, smart withdrawal planning actually begins years earlier. The types of accounts you choose to invest in today will determine how flexible and tax-efficient your withdrawals can be later.

If all your savings end up in traditional pre-tax accounts, every dollar you pull out will eventually be taxed as income. But if you build a mix of some in Roth IRAs, some in traditional IRAs, and some in taxable brokerage accounts, you’ll have options. You’ll be able to decide where to draw from each year based on what keeps your tax bill the lowest. That flexibility can make a huge difference when market conditions change or your income fluctuates in retirement.

The withdrawal sequence still matters, of course. As a general rule, many advisors suggest starting with your taxable accounts first, then tapping your traditional IRA, and saving your Roth IRA for last. But each situation is unique, and “rules of thumb” can be deceiving.

Where Keen Capital Comes In

This kind of planning doesn’t happen overnight. It requires looking years ahead, modeling future income needs, tax brackets, and even potential changes to the tax code. That’s where professional guidance can make all the difference.

At Keen Capital, we help clients structure where they save and how they invest so that when the time comes to withdraw, it’s smooth and tax-efficient.

Whether you’re in the middle of your career or approaching retirement, the best time to plan your withdrawal strategy is now. By taking a proactive approach, you give yourself more choices later and more control over how much of your wealth stays in your pocket.

Schedule an introductory call with us today. We’ll help you make smarter, more tax-efficient decisions for your wealth, your family, and your future.